Trick or Treat?

Washington treats the economy with stimulus candies, fueling a stock market sugar high. In the long-term all that candy will not be good for the health of the economy or the market.

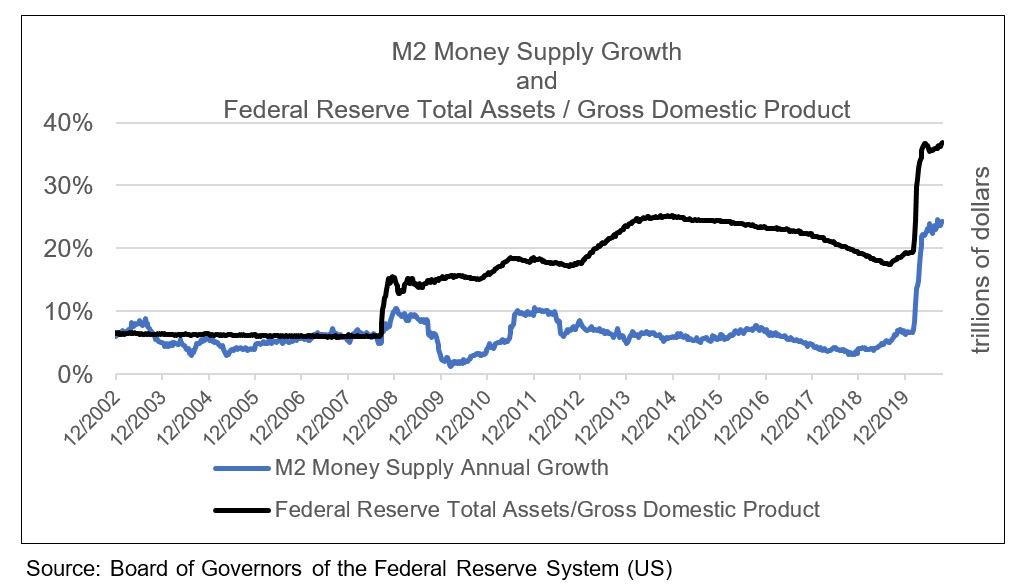

As COVID-19 accelerates into cold and flu season, it increases the likelihood of another milder slowdown followed by more deficit spending, financed through balance sheet growth at the Federal Reserve (Fed) (see chart). Historically, the U.S. has successfully deficit spent through pandemics, wars and other crises, but never has it attempted to do so when already so fiscally compromised.

For decades GDP grew and the Fed kept its asset levels fairly steady. Today, Treasury debt levels and issuance appear to have drifted beyond “crowding out” private markets to overwhelming them. On October 14, 2020, Randal Quarles, Federal Reserve Vice Chair for Supervision said:

“…(T)he Treasury market being so much larger than it was even a few years ago, much larger than it was a decade ago…(its) sheer volume…may have outpaced the ability of the private market infrastructure to support stress of any sort there…

Will there be some indefinite need for the Fed to provide…a way of supporting a functioning market in Treasuries — to participate as a purchaser for some period of time? I haven’t concluded that that’s the case…. but I do think it’s an open question.”

Following 2008, the Fed’s balance sheet grew massively without any commensurate increase in GDP; however, those increases did not cause a corresponding and potentially inflationary growth in money supply of this magnitude.

Whistling Past the Graveyard

Monetary theory tells us that it takes about a year for the full effect of a given policy approach to be felt. Many recipients of the Fed’s largess sit hording their candy buckets, waiting for loan forgiveness and a vaccine. When that spending of the Fed’s confectionary treats finally takes place, the ensuing inflation and the Fed’s efforts to take the candy away could create a truly spooky scenario for stocks.