House Rules

On April 28, 2024, a Wall Street Journal headline asserted that “Even if the Fed Cuts, the Days of Ultralow Rates are Over.” Disappointingly, the article was not about actual interest rates at all but about “R-Star,” i.e., anyone’s best guess at the real short-term interest rate expected to prevail when an economy is at full strength and inflation is stable. As you might guess, R-Star has been rising.

In identifying the potential reasons for the recent rise in R-Star, the article only once mentions the deficit. Instead, senior economists seem surprised the economy remains strong despite two years of restrictive monetary policy. Deficits matter. The author, the WSJ’s “Fed whisperer” Nick Timiraos, is quite capable and appears to have very good sources at the Fed. However, the omission of deficit spending feels like “inside-the-Fed thinking” since the Fed tends to avoid conversations about fiscal policy in order to appear politically neutral.

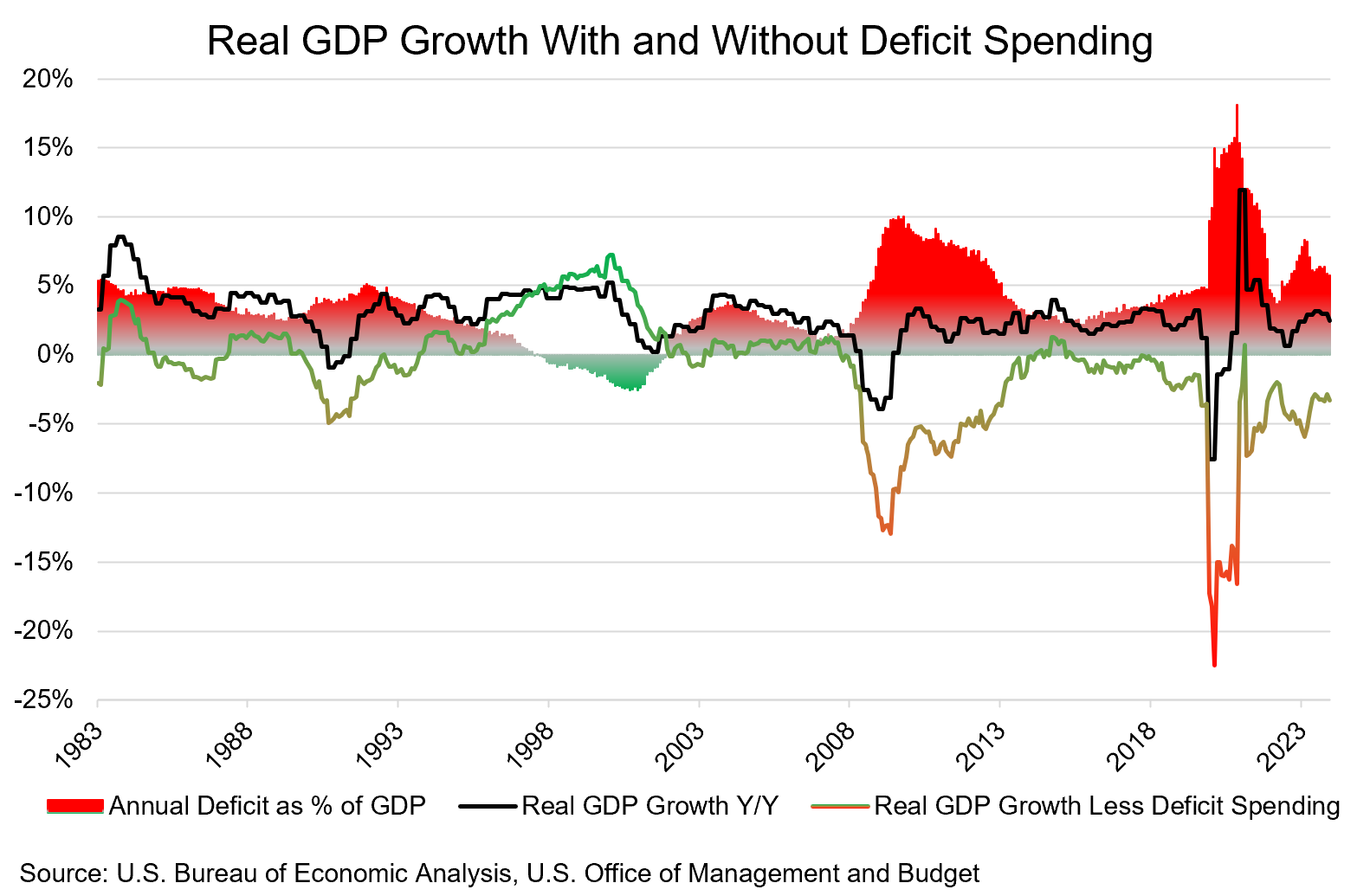

A look at Real Gross Domestic Product (economic activity after inflation) before and after federal deficit spending reveals that during the 4.25 years ending March 31, 2024, federal deficits averaged $2.2 trillion per year. The deficit during the last 12 months ending March 31, 2024 was $1.7 trillion. These numbers, 3x-4x the average $0.6 trillion seen in the six years preceding COVID-19 (2014-2019), are staggering. They are the primary reason for the lingering inflation. Unlike monetary policy, which takes years to unfold, deficit spending creates economic activity (Gross Domestic Product or GDP) in real time. The bureaucratic class borrows then spends on our behalf, pulling future spending into the present and instantly creating GDP without creating any new net wealth.

Since the beginning of COVID-19, real GDP growth has averaged 2.1% annually while deficit spending has been 9.0% of GDP. One can rightly assume that without the deficit spending, real GDP growth would have been negative, perhaps around -6.9% all things being equal. Perhaps this was attributable to COVID-19. However, over the last 12 months ending March 31, 2024, if not for deficit spending equal to 5.9% of GDP, the 3.0% growth in real GDP might have been roughly -2.9%. Our economy is not growing, but is instead destroying wealth when viewed net of inflation and debt issuance. Increasingly, real GDP is positive only because of fiscal deficit spending, a grim reality.

Using debt-fueled spending to maintain GDP is not new, but the problem is getting worse at a quickening pace. Averaging the six years before COVID-19, after deficit spending of 3.3% of GDP, real GDP grew at 2.5%, a decline of -0.7% in real GDP net of deficit spending. If we were to adjust the numbers for our growing population, the resulting “per capita” numbers of recent years would look incrementally worse.

Looking further back, one can see it has not always been this way. During the 25 years preceding the Great Financial Crisis, real GDP growth averaged 3.4% per year. After subtracting 2.3% in deficit spending, the annual growth of real GDP before any assistance from government borrowing and spending averaged 1.1%. Most of U.S. history is one of positive GDP growth net of inflation and debt issuance.

Protection Racket

Governments too often seek to protect themselves, working at cross-purposes with—rather than seeking to promote—real per-capita wealth creation by the private sector. The U.S. is now living through a slow-motion train wreck at the hands of both political parties, the administrative state, lobbyists, and the media. They win while the country loses.

Over 20 years ago, Robinson Value Management set out to make government-awareness a major factor in our investment strategies. The federal government is the largest borrower and purchaser of goods and services on the planet. It leaves large footprints, picks winners and losers, adds and removes uncertainty through ordinary policy-making, and controls liquidity in markets. Like any large bureaucracy; it appreciates predictability and certainty, has mandates which must be met, and may be increasingly vulnerable to its growing size.

In a card game, if you do not know who the patsy is, then you are it. Sophisticated investors should consider ways to make government the patsy, i.e., to seek to manage, benefit from, and mitigate risks created by the largest and most powerful economic entity on earth as it seeks to protect itself.